What is involuntary churn?

Involuntary churn — also called passive churn or payment failure churn — is when a subscription is cancelled because of a technical payment failure rather than a deliberate customer decision. The customer didn't log in and click "Cancel." Their card just stopped working, and the subscription lapsed.

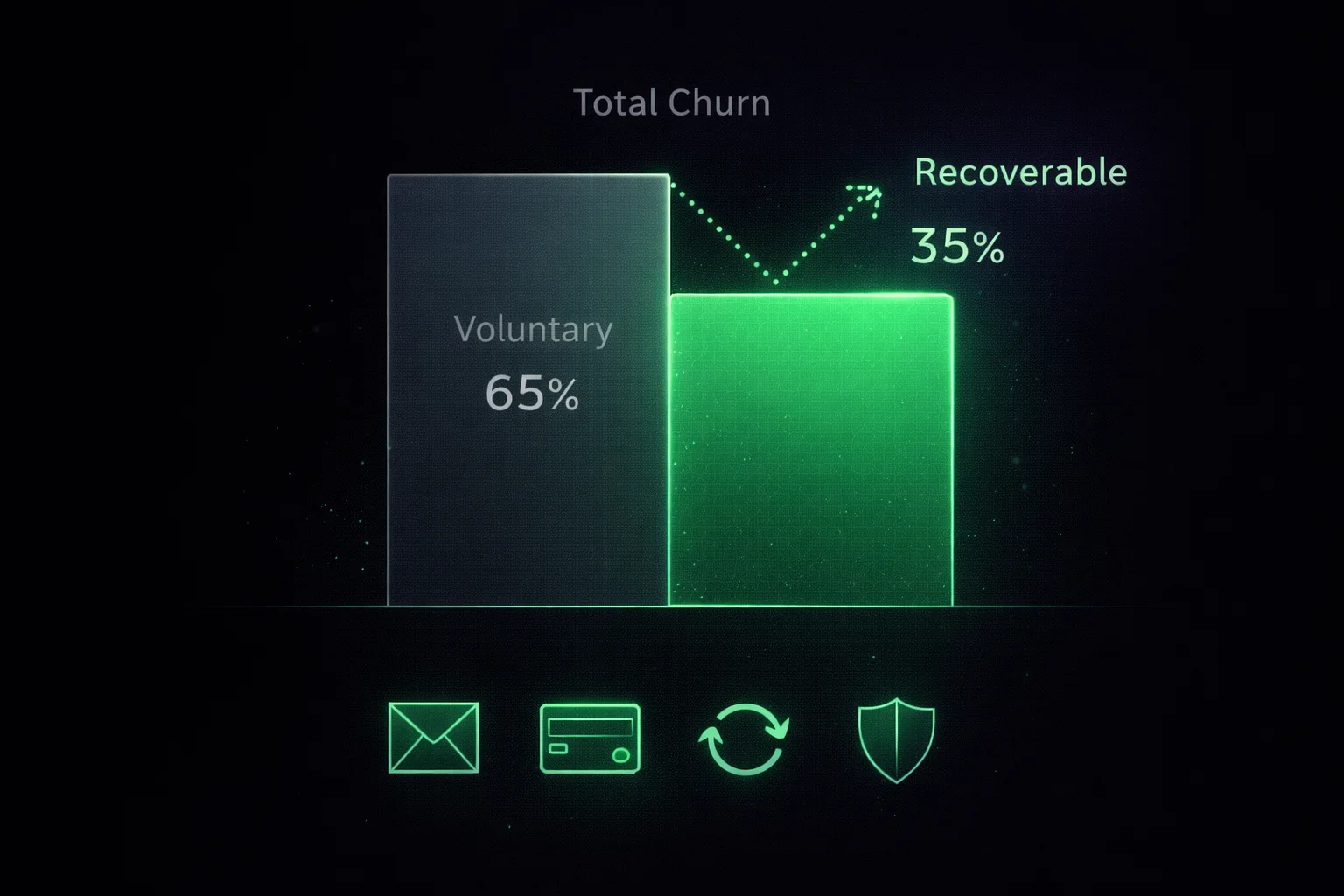

This is different from voluntary churn, where a customer actively cancels because they no longer want the product. Voluntary churn requires product, pricing, and retention work to fix. Involuntary churn is a billing infrastructure problem — and it's nearly entirely recoverable with the right systems.

Why it matters more than you think

Most SaaS founders focus their churn reduction efforts on the customer experience — improving onboarding, reducing friction, building features. That's correct for voluntary churn. But if 30% of your cancellations are happening because of expired cards, all the product improvements in the world won't touch that number.

The other reason involuntary churn is underestimated: it doesn't look like a decision. There's no cancellation event in your analytics, no exit survey response, no angry email. The subscription just silently lapses. Many SaaS companies only discover how much involuntary churn they have when they run a cohort analysis and find a large share of "cancellations" had no user-initiated cancel event.

At $20,000 MRR, if 2.5% of subscriptions lapse monthly due to payment failure, that's $500/month — $6,000/year — in preventable revenue loss. A dunning tool that costs $59/month and recovers 50% of those failures pays for itself many times over.

8 tactics to reduce involuntary churn

Ordered by impact. Start with tactic 1 — it's the highest-ROI action available and takes an afternoon to set up.

Set up a dunning email sequence

A dunning email sequence is a timed series of messages sent after a payment fails — notification on day 0, reminders on days 3 and 7, a backup card ask on day 10, and a final warning on day 13. Each email creates another chance for the customer to fix the issue before cancellation.

Industry data shows that 40–60% of failed payments are recoverable with a proper multi-step sequence. Most of these recoveries happen in the first 7 days — which is why the immediate notification is the single most important email you'll send.

The tone matters: most failed payments aren't intentional. Treat dunning emails like helpful service notifications, not collections notices. Customers who feel blamed are more likely to churn voluntarily after the payment issue is resolved.

See 6 copy-paste dunning email templates →Use smart payment retries

Smart retries re-attempt a failed charge at an optimised time based on the decline reason. A naive system retries at fixed intervals regardless of why the payment failed. A smart system knows that "insufficient funds" (NSF) failures should be retried mid-month; "do not honour" failures should skip retries and go straight to email.

25–35% of all failed payments recover on the first smart retry before any email is sent. This is the highest-leverage, lowest-effort recovery mechanism available — and most of the work is done by the retry engine itself.

Stripe's built-in Smart Retries handle the basic case. Dedicated dunning tools layer additional logic on top — using broader decline pattern data to pick better retry windows than Stripe alone.

How MRRescue's smart retries work →Send expiring card alerts

Expiring cards account for 25–30% of all subscription payment failures — making them the single most common failure reason. The fix is simple: send a proactive alert 2–3 weeks before the card expires, giving the customer time to update before the renewal fails.

Expiring card alerts are purely preventative — they stop the failure from happening in the first place. This makes them more effective than dunning emails in one sense: the customer updates their card while still feeling good about the product, rather than in response to a payment failure notification.

Stripe provides card expiry data via the API. Building the alert sequence yourself takes time; dunning tools like MRRescue handle this automatically as part of the feature set.

MRRescue expiring card alerts →Add backup payment method capture

Some customers genuinely cannot update their primary card quickly — a replacement card is in the mail, or a corporate card needs re-authorisation. A backup payment method request asks the customer to add an alternative card as a safety net.

Adding a backup payment capture to your dunning sequence (typically at day 10) recovers roughly 15% of total recoveries — the payments that would have been missed if you only offered the primary card update path.

The psychology here is different: the customer isn't asked to fix their main card, they're asked to add a temporary alternative. This is an easier yes for many people.

MRRescue backup payment requests →Add in-app payment prompts

Email dunning is effective, but customers who are actively using your product during a payment failure are the easiest to reach. An in-app notification — a banner, modal, or top-of-screen alert — catches users while they're already engaged.

In-app prompts work best as a complement to email, not a replacement. A customer who sees a payment failure notice both in their inbox and inside the app is significantly more likely to act than one who only saw the email (which may have gone to a secondary folder).

Implementation requires adding billing state awareness to your front-end — typically by checking the subscription status on dashboard load and conditionally rendering an alert component.

MRRescue in-app recovery widget →Use account updater services

Account updaters are services run by card networks (Visa, Mastercard) that automatically update stored card details when a card is reissued, replaced, or renewed. When a customer gets a new card, the network notifies card processors with the updated card number — preventing the failure before it happens.

Stripe supports account updater for eligible cards automatically. Not all cards are eligible (mainly US-issued Visa and Mastercard), but the share of failures prevented is meaningful — typically 10–20% of expiry-related failures.

This runs in the background with no customer action required. It's one of the most passive ways to reduce involuntary churn.

Analyse payment failure reasons

Not all failed payments are the same. Stripe provides a decline reason code for every failure — "insufficient_funds", "card_declined", "expired_card", "do_not_honor", etc. Analysing which reasons drive your failures tells you where to invest in recovery.

If 40% of your failures are insufficient funds, retry timing optimisation and mid-month retry windows will have outsized impact. If 30% are expired cards, expiring card alerts should be your first priority. If 20% are hard declines, email is the only recovery option and your sequence needs to be airtight.

This analysis is easy to run with a simple Stripe API query grouped by decline reason. Dunning tools with analytics dashboards surface this automatically.

MRRescue analytics and risk scoring →Run win-back campaigns for lapsed subscribers

When a subscription does lapse despite your dunning sequence, a win-back email sent 30–60 days later can still recover 10–20% of those accounts. Many lapsed customers experienced a temporary issue — the card was sorting itself out, a bank dispute was being resolved — and will return if you make it easy.

The win-back email works because it reframes the situation: it tells the customer their data is still there, that you'd love to have them back, and that reactivation is one click away. There's no accusation, no urgency pressure — just an open door.

Win-back campaigns are systematically underused because most teams focus only on the active dunning window. Adding a 30-day post-lapse email to your sequence is low effort and consistently generates positive ROI.

MRRescue win-back campaigns →All 8 tactics, automated in one tool

MRRescue covers dunning sequences, smart retries, expiring card alerts, backup card capture, win-back campaigns, and analytics — all connected to Stripe in 5 minutes.

Start free — no credit card →Related reading

What is dunning?

The full explainer on what dunning is and why SaaS companies need it

6 Failed Payment Email Templates

Copy-paste dunning emails with subject lines and timing

Best Dunning Software for SaaS in 2026

Head-to-head comparison of the leading tools

MRRescue: Failed Payment Recovery

How automated dunning works for Stripe SaaS

Stripe Decline Codes Explained

Every decline code, retry strategy, and recovery email approach

Frequently asked questions

What is involuntary churn?

Involuntary churn is when a subscription is cancelled because of a failed payment rather than a deliberate decision by the customer. Common causes include expired cards, insufficient funds, and bank-side fraud flags. Studies estimate that 20–40% of all subscription cancellations are involuntary.

What's the difference between voluntary and involuntary churn?

Voluntary churn occurs when a customer intentionally cancels their subscription — typically because they no longer see value in the product. Involuntary churn happens passively when a payment fails and the subscription lapses without the customer intending to cancel. Involuntary churn is recoverable with dunning; voluntary churn requires product and retention improvements.

How much MRR can I recover by fixing involuntary churn?

A complete dunning system can recover 40–60% of failed payments. At $10,000 MRR, if 2% of subscriptions lapse monthly due to payment failure, a 50% recovery rate is worth $100/month — $1,200/year. The ROI on dunning software is typically achieved within the first 30–60 days.

Does Stripe handle involuntary churn automatically?

Stripe includes Smart Retries and one configurable email. This recovers some involuntary churn but misses a significant share. A full dunning sequence (multiple emails, backup card capture, expiring card alerts, win-back campaigns) recovers substantially more. Dedicated dunning software layers these capabilities on top of Stripe.

What's the most important thing to do first to reduce involuntary churn?

Set up a dunning email sequence immediately after payment failures — starting with a same-day notification. This is the single highest-ROI action because it catches customers while the issue is fresh and recoverable. Beyond that, adding expiring card alerts (sent 2–3 weeks before card expiry) prevents the failure from happening in the first place.

Start recovering failed payments today

MRRescue automates every tactic in this guide. Connect your Stripe account in 5 minutes — free 14-day trial, no credit card required.

Start free →